Sustainable Water Management: The Tide is Turning

Investor interest in water-related issues is on the rise with investors such as Norges Bank Investment Management stating that "water scarcity on a global scale represents a financial risk to the fund. Economic growth, industrialization and population growth are driving the increasing demand for water, while factors such as climate change, pollution and regulation are affecting the supply and costs related to water." The chemical industry, being highly water intensive, certainly is exposed to water-related risks. Any efforts to manage these risks and capitalize on opportunities begin with the measurement and appreciation of how water may impact business, followed by the development of strategies to protect the business both now and in the future.

The Carbon Disclosure Project (CDP) (www.cdproject.net), London, an international not-for-profit organization, has worked with large companies around the world for over a decade, helping to accelerate awareness and management of environmental risk. It pioneered the only global system that collects information about corporate behavior on water security and climate change. CDP's water program focuses specifically on mobilizing positive and tangible action on sustainable water management by enabling businesses, investors and policy makers to better understand the corporate risks and opportunities associated with water scarcity and other critical water-related issues.

CDP's goal of enabling better decision-making by providing high quality information on how companies are managing their responses to natural resource constraints has never been more important. Demonstrating the growing significance of water management as an investment issue, the 2012 CDP request for information on water, which was sent to 318 of the world's largest companies listed on the FTSE Global Equity Index Series (the Global 500), was formally supported by 470 investors representing $50 trillion in assets.

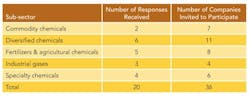

CDP received responses from 20 companies in the chemical industry. A total of 36 companies in five chemical sub-sectors were asked to respond — see Table 1. The response rate of just 56% was disappointing given the weight of investor interest in the issue and the increasing proportion of companies across all industries reporting water-related impacts, risks and opportunities.

• Almost two-thirds of chemical industry respondents have experienced water-related negative impacts to their business in the past five years, and the majority of respondents have identified water as a substantial and current risk to their business.

• Encouragingly, the majority of respondents report that water represents a current strategic opportunity to improve their financial and brand performance, with some opportunities having sales potentials of more than €800 million ($1 billion) by 2020.

• Despite this, less than half of respondents have set concrete targets or goals with regard to water-related issues, suggesting that water isn't receiving strategic attention proportionate to its risks and opportunities.

A GROWING AND IMMINENT RISK

Water risk is a prominent issue among chemical industry respondents. Indeed, 65% report suffering water-related adverse business impacts in the past five years — this is significantly higher than the full Global 500 sample average (53%). Impacts include business interruption through the closure of major transport routes and property damage. DuPont's operations, for example, were affected by storm surges and flooding associated with major hurricanes in 2008.

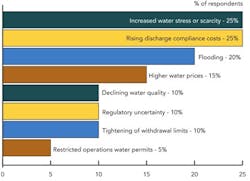

Perhaps as a result of this, 70% of chemical respondents identify water as a substantial risk to their business, either in their direct operations or across their supply chains. Increased water stress/scarcity, and regulation of discharge quality/volumes leading to higher compliance costs are the most frequently reported risks (Figure 1). This perhaps isn't surprising given the inherent nature of the chemical industry and the hazards that some chemicals pose to humans and the environment. For example, DSM states that reputational damage resulting from water-related issues can negatively impact shareholder value and that water-related incidents can lead to severe business interruptions.

Given that the majority of the risks identified are reported to have the potential to impact businesses now or within the next five years, there is clearly an urgent need for companies to develop effective management responses.

Israel Chemicals provides a compelling example of the critical nature of a sustainable supply of water to business continuity. The company depends upon the Dead Sea as a significant source of raw materials, yet due to historic and current extraction practices, the sea's water level is dropping at a rate of around one meter per year. Solutions proposed by the Israeli Government are likely to affect the composition of the sea water and, hence, the quantity of materials the company can produce. It's anticipating "significant expenses" as a result.

The supply chain features frequently as a significant source of risk among Global 500 companies. However, only 15% of chemical industry respondents report that water-related risks within their supply chain have the potential to substantively impact their business. Nonetheless, 50% of the identified risks, including reputational damage, increased water stress/scarcity and flooding, are anticipated to impact businesses now or in the next five years.

Of those companies noting they aren't exposed to supply chain risks, the majority, including Dow, DuPont and Potash, explain that their strategy of multiple-sourcing enables them to circumvent any risks. Other firms, such as Air Liquide, Ecolab and Syngenta, rely on supplier engagement to mitigate risks.

Worryingly, however, over a third (35%) of respondents are unable to state whether or not they are exposed to risks across their supply chain. Many cite the sheer number of suppliers as a barrier to understanding these risks; others report they traditionally have focused on risks across direct operations but are in the process of broadening their analyses to cover supply chains.

Encouragingly, respondents are taking steps to address the uncertainty around supply chain risks, with 35% requiring key suppliers to report their water use, risks and management. It is recommended that other chemical companies consider engaging their key suppliers on water-related issues.

SEIZING OPPORTUNITIES

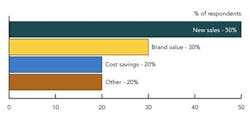

Water-related issues present substantive opportunities for their business say 80% of chemical industry respondents, a level somewhat higher than the Global 500 average (71%). These companies report a total of 43 opportunities — including creating new sales, enhancing brand value and saving costs (Figure 2) — all of which are expected to materialize within the next five years. To capitalize on these opportunities, many companies pursue water stewardship strategies that not only build business resilience, but also turn risk management responses into a source of competitive advantage.

Half of the respondents, including Akzo Nobel, Israel Chemicals and Air Products & Chemicals, foresee sales of new water-related products and services across diverse markets ranging from consumers to a variety of industrial sectors. The market should grow fastest in areas lacking access to safe drinking water and sanitation, as well as those expecting greater impacts from climate change, where water efficiency, recycling and reuse are expected to become increasingly important.

BASF, for one, provides a range of products to meet current and future water needs in terms of production, use and purification. The company estimates these products have the potential to generate more than €800 million ($1 trillion) in sales through 2020.

A number of respondents cite the cost implications of the research and development, regulatory and marketing resources required to develop, test, market and sell new products and services. However, they also note the benefits include significant opportunities to increase their market share as a result of newly developed technologies.

ADDRESSING CHALLENGES

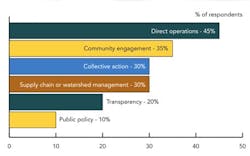

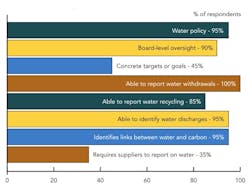

A clear and urgent need exists for the chemical industry to develop effective management responses to water-related issues. Not surprisingly, companies are focusing most on their direct operations rather than on aspects that might better address some of the underlying issues related to water scarcity, such as community engagement or watershed management (Figure 3). Almost all have developed water policies (Figure 4). All are able to report their water withdrawals and nearly all can identify their discharges. However, only 45% have established specific water-related targets or goals. This is much lower than expected considering the proportion of companies that have already experienced water-related negative business impacts.

Moreover, many of these targets focus on the efficient use of water (recycle and re-use) and reducing water consumption in general rather than on water quality management. This is surprising considering one of the risks chemical industry respondents most frequently cite is increasing regulation of discharge quality.

Praxair is using the WBCSD Global Water Tool to build a picture of water stress or abundance both now and over the next 15 years. It plans to use the findings as a basis to improve water management and reporting across the entire company.

Israel Chemicals has established an "ecological tax" — an intra-organizational tool that adds effluent treatment costs onto the total price of a product. This provides an incentive for production managers to reduce the quantity of pollutants and effluents at the source in addition to acting as a tool for estimating the "environmental" price of each product.

Taking collective actions to address water-related issues is becoming more popular. Chemical industry respondents are beginning to realize that no single company can address some of the underlying water challenges. So, for example, DuPont is taking part in the Aqueduct project of the World Resources Institute, Washington, D.C. This project's objective is to "equip and motivate companies operating in water-stressed regions to minimize their water consumption and other impacts, drive markets for environmentally sound hydro technologies, and advance economic development without threatening freshwater resources in their communities."

Meanwhile, Syngenta, recognizing the challenges it faces in offering timely advice on optimum agronomy solutions for crops to farmers spread over large, sometimes remote, areas, has teamed up with Nokia. "Syngenta has been working with Nokia LifeTools to set up an easy-to-use, graphical interface that works anywhere on Nokia cell phones. With this wireless application, Syngenta can provide growers with crop-specific tips on pest and disease management."

TAKE PART IN THIS YEAR'S SURVEY

Disclosing water-related information has the potential to create value and mitigate operational, regulatory and reputational risks. CDP's water questionnaire is sent to the world's largest companies in sectors that have the greatest potential to impact or be impacted by water resource issues globally. The organization continues to expand its global reach and currently targets companies from these sectors that are in the FTSE Global Equity Index Series (the 500 largest companies globally), the S&P 500 (the 500 largest U.S. companies), the ASX 100 (the 100 largest Australian companies) and the JSE 100 (the 100 largest South African companies). All companies are welcome to respond whether or not they appear on these rosters. Please contact [email protected] to register as a voluntary discloser. Deadline for 2013 disclosure is June 27.

CATE LAMB is head, CDP Water Disclosure, for the Carbon Disclosure Project, London. E-mail her at [email protected].