The global economy has reached a critical state. In early 2011 the recovery had entered its third year but the pace of improvement slowed as higher energy prices, the disasters in Japan, the Eurozone crisis and the influence of other negative factors spread. A global soft-patch emerged — one centered in manufacturing. Unfortunately for the chemical industry, the manufacturing sector represents its major end-use or customer base.

Dynamic growth has occurred in China and in other emerging markets where recovery evolved into business cycle expansion during 2010. However, in the United States and other developed nations, a typical business-cycle recovery has yet to appear in many sectors. Although US gross domestic product (GDP) surpassed its pre-recession peak in the 3rd quarter of 2011, growth remains slow as of this writing (late November). Business investment and exports have been drivers but recent indicators suggest the robust manufacturing recovery in the United States has lost momentum. Of the nearly nine million US jobs shed during the "great recession," less than one third have returned. High unemployment persists, personal incomes now are shrinking, and Americans continue to be burdened by high debt levels and the impact of lower home prices on household wealth. The nation is in its fourth year of a seven-year deleveraging (of debt) cycle, and an anemic recovery, typical of that from a financial crisis, is the norm.

The consensus forecast (our base-case scenario) for US GDP is for continued but anemic growth through 2012, at a level well below the historic trend. The current "soft-patch" could very well be a typical mid-cycle slowdown, in which case a rebound of activity should emerge. However, economic growth likely won't reach long-term trend levels until 2013. The recovery is fragile, though — multiple risks remain and the likelihood of another recession is high. The wrong trade, tax or other policy initiatives could derail activity.

Temporary supply-chain disruptions from the disaster in Japan slowed growth, adding to the drag from higher oil prices. The European debt crisis continues to present one of the greatest risks to the world economy, as does uncertainty about US debt levels, policy and long-term economic prospects. The stability of the banking system in China is raising concerns in light of massive credit inflation and exposure to real estate and local government loans. Any of these could combine to foster another recession. Prospects going forward represent a two-speed world in which the developed nations (constrained by debt and adverse demographic factors) grow slowly while the emerging markets grow rapidly as a result of industrialization and rising consumer-driven economies.

PROSPECTS FOR CHEMICALS

Most major end-use markets for chemicals, especially those tied to export markets and business investment, have recovered in the United States. The manufacturing sector, which is the largest consumer of chemicals, strongly rebounded during the recovery but growth has slackened as demand has weakened. Industrial output remains below its pre-recession peak in the United States and activity slowed in the 3rd quarter.

A two-speed manufacturing sector, with about one-half of industries soft and others doing well, has emerged. The boom in oil and gas is creating opportunities both on the demand side (e.g., for pipe and oilfield machinery) and the supply side (e.g., for chemicals, fertilizers and direct iron reduction). There's strength in light vehicles and aircraft as well as in industries involved with business investment (iron and steel, foundries, computers, etc.), and a recovery in construction materials. Elsewhere, structural issues are sapping dynamism in a number of industries (textiles, paper, printing, etc.). Forward momentum depends upon demand for consumer goods, which ultimately drives factory output. However, weakening foreign demand (chemicals are early on in supply chain and exports to Europe have evaporated) presents challenges for the manufacturing sectors. Balance sheets are strong and lower raw material costs have benefited manufacturers. Nonetheless, an uncertain business and regulatory environment is constraining business optimism — and hiring.

Light vehicles represent an important market for chemicals (nearly $3,000 per vehicle), and production has experienced temporary disruptions from the disaster in Japan. US light vehicle sales should rise to 13.5 million units in 2012 as pent-up demand fosters growth. Sales will improve even further during 2013, exceeding 14.5 million units then.

However, housing, the other large consumer of chemicals (over $15,000 per start), faces ongoing challenges. New homebuilding remains depressed as foreclosures continue to flood inventories. Only a minor gain in housing starts should occur in 2012 and the recovery in this sector will be quite slow. Housing activity should begin to stir in 2013. It remains well below the previous peak of 2.07 million units in 2005 and below the long-term underlying demand of 1.5 million units per year as suggested by demographics and replacement needs. Unfortunately, today's massive housing inventory will delay a full recovery until later this decade.

The softening of the manufacturing recovery should dampen chemical demand. Inventories can mean the difference between a slowdown and a recession; in general, lean inventories along the supply chain support future production gains. U. S. chemical inventories are relatively balanced and, barring a major recession, a large correction isn't expected. Production of chemicals, excluding pharmaceuticals, has eased as demand from key end-use markets has slowed and capacity utilization remains relatively stagnant (see Economic Snapshot, p. tk). Chemical exports continue to grow — driven by overseas growth, a weaker dollar and a favorable oil-to-gas price ratio.

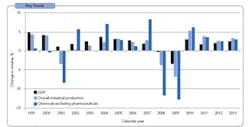

The consensus is that US chemical output should improve slightly during 2012. Volumes for chemicals, excluding pharmaceuticals, which rose 6.1% in 2010 and should show a 3.5% gain in 2011, likely will grow only 2.5% in 2012 but then recover to 3.0% in 2013. Robust growth is expected in synthetic rubber and later in petrochemicals, organic derivatives and plastic resins as export markets revive. Demand from end-use markets will drive production of specialty chemicals. Strong gains are expected in agricultural chemicals and consumer products. In the long term, chemicals growth should expand at a pace exceeding that of the overall US economy (Figure 1).

THE IMPACT OF LOW-COST GAS

American chemical makers likely will strongly increase capital spending during the next several years. The need to add capacity and improve operating efficiencies will play a role. However, plants for petrochemicals and derivatives based on shale gas should account for a lot of the investment.

Vast new supplies of natural gas from previously untapped shale deposits represent one of the most exciting domestic energy developments of the past 50 years. After years of high and volatile natural gas prices, the new economics of shale gas are a "game changer," creating a competitive advantage for US manufacturers, leading to greater investment and industry growth.

Expansion of domestic shale gas production is helping to reduce US natural gas prices and create a more stable supply of natural gas for fuel and power creation. This benefits all American manufacturers.

However, lower natural gas prices offer an important additional advantage to chemical makers because they can use the gas as a raw material or feedstock. In the United States, historically it's been cheaper to crack ethane, propane and other natural gas liquids than to crack naphtha (from oil refining), the primary petrochemical feedstock in Western Europe and Northeast Asia. The ethane steam-cracking process is simpler and its hardware is less expensive. Nearly 90% of North American ethylene now comes from natural gas liquids. US ethane prices correlate (0.82) with the Henry Hub natural gas price and Western European naphtha prices highly correlate (0.97) with the Brent oil price. So, feedstock costs — and competitiveness — significantly depend on gas and oil prices.

Not that long ago, many industry observers were writing off petrochemicals from the US Gulf Coast (USGC). Production there was far more expensive than in Western Europe and Northeast Asia. A pending wave of capacity in the Middle East only added to dour sentiments. However, the revolution in shale gas has changed USGC economics radically for the better. By 2010, the USGC had become second only to the Middle East for low production costs. Moreover, ethane supplies are tightening in the Middle East and are constrained; the era of low-cost feedstocks in that region soon may be over.

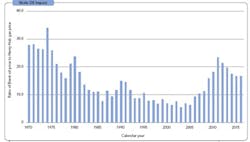

As a rough rule of thumb, a ratio of Brent oil price to Henry Hub natural gas price above a band of 6:1 to 7:1 enhances the competitiveness of USGC-based petrochemicals and derivatives such as plastic resins compared to other major producing regions. (Other factors such as co-product prices, exchange rates and capacity utilization play a role in competitiveness as well, of course.) As a result of shale gas, this important ratio has exceeded 7:1 for several years and recently has surpassed 25:1, which is very favorable for US competitiveness and exports of petrochemicals, plastics and other derivatives (Figure 2). This has led to strong gains in US plastics exports. Such exports have stabilized, though, but mainly because of the crisis in Europe and weakness in that region's economy. Some capacity constraints have occurred and rising North American demand for plastic resins has cut into exports.

The impact of abundant low-cost shale gas now extends beyond petrochemicals to production of other chemicals including fertilizers and downstream products. Companies are reconsidering capital investment in North America and have announced a slew of projects. With a recovery in Europe's economy, the startup of some of these projects and sustained competitiveness, the outlook for North American exports of plastic resins is quite good in the medium and long term. In turn, this will generate new business and, importantly, jobs.

WHAT COULD GO WRONG?

Many forecasters are concerned about an outright downturn, i.e., a recession, in the US economy. Certainly the higher energy prices and the supply chain shock emanating from Japan earlier in the year, as well as continued weakness in housing, the European debt crisis, US debt issues, uncertainty and other factors are working against the recovery. And other risks lurk in the background. A combination of these could engender a vicious cycle of financial distress, asset depreciation, and falling incomes, sales, production and employment. These challenges potentially could push the global economy back into recession. Most notable is the European debt crisis and the emerging recession there, which would adversely affect US exports and our economy and, should a financial crisis emerge, definitely tip the United States into recession. The odds of a recession are about 40%. Should another downturn occur, US chemicals output excluding pharmaceuticals, instead of growing roughly 2.5% in 2012 would likely decline 3%!

The economy clearly is at a critical juncture, but most forecasters expect the recovery to progress, although at an anemic and at times uneven pace. Let's hope the consensus scenario comes to pass, but the prudent observer will prepare for the alternative scenario as well.

THOMAS K. SWIFT is chief economist and managing director of the American Chemistry Council, Arlington, VA. E-mail him at [email protected].